How to Actually Spend Crypto in Real Life

Note from the editor: A lot of people ask me about private payment options. The existing financial system is a surveillancescape. If you want privacy, you can’t really use traditional payment rails. Masked credit cards will let you hide your identity from merchants, but the card issuer is still required under the Bank Secrecy Act Regime to KYC you, retain your transaction history, and make it accessible to more than 25,000 federal, state, and local government users through the FinCEN Query Program — all without a warrant. Basically every casual transaction between ordinary Americans is accessible to the federal government. Traditional payment rails constitute one of the largest warrantless financial surveillance apparatus in the country, and it sweeps in every American who uses a bank or an app. This surveillance is a global phenomenon, not isolated to the USA.

To avoid this, your other options are cash, gift cards, or cryptocurrency. A lot of people avoid cryptocurrency because they don’t see it as useful — it doesn’t seem like there’s anywhere to spend it. The guest post below was written by Violet Rollergirl. She helps people in vulnerable communities adopt privacy tools, including private payment methods. Hopefully this article will be helpful if you want to know how you can actually use crypto in daily life, and reclaim financial privacy.

To be clear: there's nothing illegal about using cryptocurrency or opting out of traditional financial surveillance. Choosing private payment rails is a normal exercise of financial liberty — the same one every cash transaction has represented for centuries.

Yours in Privacy,

Naomi

Off-ramping: where and how to spend your cryptocurrency

By Violet Rollergirl

At the end of the day, cryptocurrency is just currency. Sooner or later, you’re going to have to spend it on something.The cryptocurrency world calls this “off-ramping,” and it means turning your cryptocurrency assets into something else, whether digital or physical.In the traditional financial system, spending money comes with a privacy trade-off: your bank, credit card company, and payment processor know what you’re up to. Transparent (non-private) cryptocurrency systems suffer from the same problem, but worse, because everyone in the entire world can watch what you buy. This is one of the main safety benefits to using privacy coins: no one but you and the vendor you’re buying from knows what you’re up to.

Paying directly in cryptocurrency

The easiest way to off-ramp or spend your cryptocurrency is to just pay for the thing in the same privacy coin you already have. Of course, this requires the vendor to accept payments in that privacy coin, and that’s still rare. [If someone in your community] is willing to accept payment for a service in Zcash, I’ve got my perfect off-ramp right there!So if you’re a gig worker with skills, share that fact with friends you trust. Build a local economy, and stay surveillance-free by using something like Zcash to sustain it! The true revolutionary potential of this truly cannot be overstated.One way to think about this is: Zodling Zcash is to money what using Signal is to speech. Vive la révolution!

Paying in Bitcoin when you only have Zcash

Although Zcash is a superior private currency, most of the crypto world still relies on other surveillable systems, like Bitcoin. Thankfully, cryptocurrencies can be easily converted from one to another so it’s easy to pay in a vendor’s cryptocurrency of choice even if you only keep a balance in Zcash. There are lots of ways to do this, but many are clunky and require you to be quite careful about exchange rates, conversion fees, and payment processing times.

By far the easiest method is Zodl’s “Crosspay” feature, so named because it can make “cross-chain payments” simple and safe. Let’s work through a common use case I have one step at a time and show Crosspay at work.

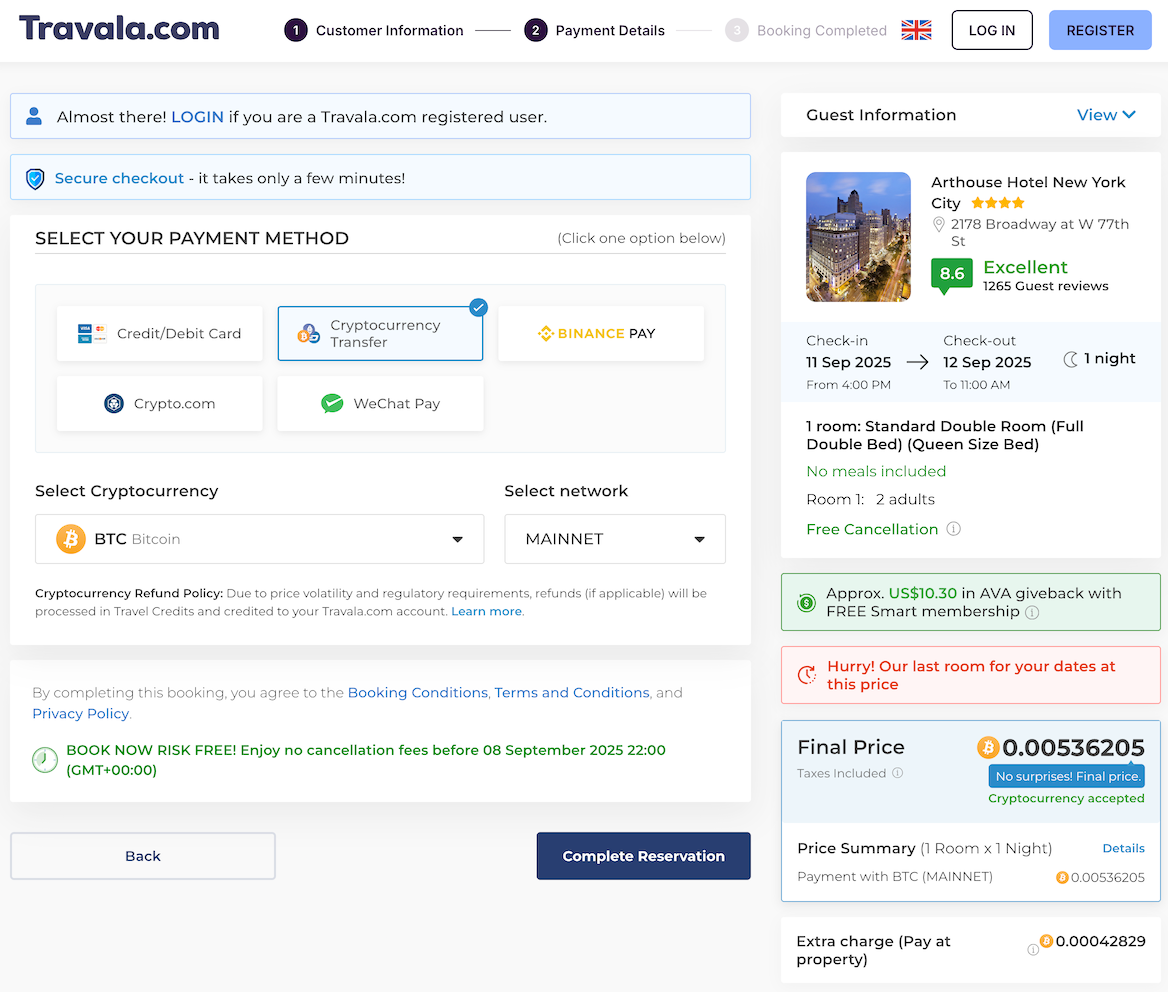

As a person who travels frequently, one very common need I have is to pay for my travel bookings. Some newer travel sites will accept payment in Bitcoin, Ethereum, or other cryptocurrencies, but I’m aware of none who accept Zcash. (Obviously, if you know of one, please contact me to tell me about it!) This is where Zodl’s Crosspay feature shines and where Travala comes in clutch.

It works like you’d expect any other flight and hotel booking platform to work, but you can pay directly in cryptocurrency. They also have a loyalty program, so you can earn extra rewards, and help me do the same if you sign up via my referral link.

Travala’s payment options include direct cryptocurrency transfer with dozens upon dozens of different supported cryptocurrencies, including the popular ones. While Travala doesn’t support Zcash directly, Zodl lets you swap your ZEC out for a number of cryptocurrencies that Travala does support at the same time as you send a payment.

To pay for a hotel booking or flight ticket with cryptocurrency:

Start at Travala and find the hotel or flight you want to book just like any other travel website.

Once on its checkout screen, choose a cryptocurrency to pay in and begin the checkout process. Travala will present a checkout screen to you that looks something like this:

When you’re ready to pay, proceed to the payment screen itself, which will give you a QR code or address to copy.

Copy the address presented to you.

Open your Zodl wallet app.

Click on Zodl’s “Pay” button to open the Crosspay screen.

Next, in the “Send to” section, enter the payee’s (Travala’s) information:

You’ll see a cryptocurrency selection drop-down menu for choosing the currency the payee wants to receive from us. Find Bitcoin (BTC) from the list of options; it will have a small Bitcoin logo on top of a larger, second, identical Bitcoin logo. This means we’re using our shielded ZEC, but paying in Bitcoin.

In the Address field, paste the Bitcoin payment address you copied from Travala earlier.

Now choose how much to pay by entering an amount in Bitcoin units.

Click “Review” at the bottom of the Zodl Crosspay screen. Zodl’s “Pay Now” drawer will open.

Review your payment and ensure that the amount will cover your order.

Click “Confirm” when you are ready to make your payment and send the transaction.

In my experience, it takes about 5 to 10 minutes for the transaction to complete, so make sure you also have at least that much time on the checkout payment timer before you confirm your transaction, or you may not be able to get your account credited before your purchase order expires. If that does happen, you’ll have to speak with a support representative about crediting your account.

There’s a lot of sparkle-emoji technology sparkle-emoji happening here, but what’s extra cool about this is that at no point do you ever need a Bitcoin wallet! Moreover, no remnant of digital cruft exists anywhere in the various blockchains that can be meaningfully linked back to you.

Practically, this enables you to safely keep your cryptocurrency assets in the Zcash shielded pool, where they stay completely private, and still be able to pay any vendor who accepts any supported cryptocurrency equally privately. If you do this, no one can know how rich (or poor) you really are. In contrast, if you keep your holdings in a transparent ledger system like Bitcoin, the whole world can tally your real net worth and track your transactions without ever asking you questions.

This is not a hypothetical example. This is in fact how I pay for the VoIP phone number I use, and other services.

Piggyback on the gift card economy

Among the most common ways to spend your hard-earned cryptocurrency today is by piggybacking on the massive gift card economy for making various kinds of retail purchases. Since gift cards and store credit systems are already a certain kind of alternative digital local currency, cryptocurrency is a natural fit. As a result, an entire crypto gift card marketplace industry has emerged to support this particular kind of off-ramp. While different crypto-to-gift-card vendors support different currencies, Zodl’s built-in decentralized exchange solves that problem, so the main considerations for those of us who want to use this method to spend our cryptocurrency funds are:

finding a crypto to gift card exchange provider that partners with a brand we want to buy from, and

ensuring that the exchange provider’s terms of use and their “Know Your Customer” rules doesn’t risk our privacy more than we are comfortable with.

If you’re just starting from scratch, here are my favorite vendors — two of them conveniently, are built into the same self-custody wallets I’ve already recommended.

Pay for stuff via Flexa in Zodl

The gift card vendor directly integrated with the Zcash wallet app I use is called Flexa, which is basically a multi-store gift card manager mini-app inside the Zodl wallet app itself. If you’ve installed the mainstream version of Zodl (i.e., from the Google Play Store, the Apple App Store, or the Aurora store) you’ll have the option to spend your shielded ZEC at partnered Flexa brands from within your Zodl wallet. If you downloaded your Zodl wallet from the F-Droid strictly free software app repository, Flexa will not work in your app.

As of this writing, some Flexa partners include Ulta Beauty and Kiehl’s (cosmetic and skincare product brands), Sheetz (a convenience store and gas station chain), and Chipotle.

First, set up Zodl to work with Flexa as privately as possible by enabling Zodl’s built-in Tor network privacy features. Once that’s set up do this to use Flexa from within Zodl:

Open your Zodl wallet app. Make sure you have some ZEC in it, enough to cover the cost of the thing you’re about to buy in the local fiat currency where you’re buying it (such as in US Dollars if you’re in the United States).

Tap the “More…” button in the Zodl main screen.

Tap the “Pay with Flexa” item in the resulting list.

If this is the first time you’ve used Flexa, you’ll be asked to complete a brief registration process where you are asked for your name and email address. At this point, there are a few things you should know:

While Flexa will have this information, none of it will end up on the Zcash blockchain network nor with the ultimate merchant from which you are buying something.

Flexa doesn't require government ID verification, and as a result caps spending at $750 per week.

If you want to use an alias email address, there are many providers you can use (like Firefox Relay, SimpleLogin, and DuckDuckGo).

Once you have a Flexa account, you’ll be given a “Flexa QR code” that is basically just a barcode that participating brands can scan as a native payment. It’s that easy. But you’ll also see a “More instant payments” box at the bottom of your screen. These are “legacy Flexa brands,” which are the stores at which you need to tell the cashier that you want to pay using a “gift card” or “store credit.” To use these:

Tap the logo icon for the brand you want to pay for. This will let you create a one-time use virtual gift card and load it up using your Zcash funds.

Enter the amount you owe at the register. If the cashier tells you that your total is $20 USD, enter that amount under the brand’s logo.

Press or tap the Confirm button. A new brand-specific virtual gift card QR code will appear.

Tell the cashier you have your gift card ready. They will ask you to scan it. Do so, and you’ll have paid!

I have successfully used Flexa this way and, while it’s currently limited to supported business partners, it is by far the easiest way to spend my ZEC on real, physical stuff.

If you need something from a store that doesn’t have a Flexa partnership, you can still maybe find it from another cryptocurrency to gift card vendor.

Other cryptocurrency to gift card off-ramps

The cryptocurrency to gift card vendor I know most about is Bitrefill (referral link), because they’re one of the largest. Another popular one I use is Piggy.Cards (referral link). Another is DashPay.

They sell gift cards to a plethora of well-known brands by accepting cryptocurrency as payment for them. You can buy these even more privately by browsing the sites via Tor Browser. If or when you hit purchase limits, you can create a “basic account” with Bitrefill to get decently large spending limits ($10,000 USD per month).

These sites allow you to spend your crypto at hundreds of places, like Amazon, AirBnB, Uber, DoorDash, Apple, Walmart, hotels, airlines… the list goes on.

Use crypto-native service providers

Instead of gift cards, which is really just a roundabout way to help fiat economy vendors accept cryptocurrency without actually accepting cryptocurrency payments, there are also a class of business-to-consumer (B2C) middlemen that will accept payments in cryptocurrency and either interface with vendors on your behalf or provide services paid for in crypto themselves.

Booking hotel stays and air travel with cryptocurrency

We’ve already looked at one such off-ramp: Travala! But it deserves a mention in this section as a reminder, as well.

Buying VoIP and Cell service with cryptocurrency

There are some VoIP providers that will accept payment directly in crypto. Here’s a short list:

JMP.chat - This VoIP provider is really a hosted Jabber/XMPP (instant messaging) service with a paid VoIP gateway. You give them Bitcoin, they give you a phone number. You can even sign up and use the service over Tor for more privacy. JMP.chat deserves its own exposition, but for now, just know it’s an option if you are comfortable getting through an unusual sign-up process.

SMSpool.net - You can rent cell numbers and pay with crypto.

(Please contact me to let me know if you found any more quality VoIP and cell providers that accept crypto payments!)

Buying VPN services with cryptocurrency

Another common service many of us have need for is a reliable VPN. I have a lot of thoughts on the topic of private network technologies, which can mostly be summed up by preference for using Tor over a VPN but with that said, if you’re going to use a VPN, you should probably stick to a reputable one that you can pay for in cryptocurrency. Here are my favorite options for that:

MullvadVPN - Uses WireGuard and OpenVPN as its VPN protocols. Mullvad also accepts payments in Bitcoin.

NymVPN - Nym is a decentralized VPN and mixnet that requires a subscription to use, and you can pay for Nym with shielded Zcash.

ProtonVPN - Many providers know this company for their ProtonMail service, but Proton also accepts Bitcoin for their VPN product, which supports WireGuard, OpenVPN, and a Stealth protocol (WireGuard over TLS) for bypassing VPN blockers.

Fund a traditional payment card using cryptocurrency

A less private option to consider is a refillable, cryptocurrency-backed, payment card with a major traditional card issuer.

Since these are the equivalent of physical credit cards, you will have to upload your legal identity documents during the application process. Still, its convenience may be useful for those who simply need an off-ramp to spend their more private cryptocurrency earnings.

The biggest advantage of these cards is:

they can be used for anything a normal credit card can be used for, like rent and utilities payments, which are situations in which even prepaid Visa gift cards may not always work.

they don’t require a bank account to pay off, making this option especially attractive for those who have suffered banking discrimination and are having trouble using or opening a traditional checking or savings account.

Apply for a Payy Card, a crypto-backed Visa payment card

Payy (referral link) is a self-custodial, privacy-centered cryptocurrency wallet and payment gateway able to interface with Visa’s payment processing network. This makes Payy two things at the same time:

a digital payment app, much like a cryptocurrency version of CashApp, Venmo, or PayPal, which makes it easy to do the kinds of things you might currently be using those apps for in your civilian life (pay back friends for dinner, for example).

a Visa payment card paid for with cryptocurrency, but usable anywhere traditional Visa credit cards are accepted.

What’s appealing about Payy is that you can fund your Payy Card’s balance using either fiat currencies, such as from traditional bank accounts, or cryptocurrency sources, such as other crypto wallets or exchanges, by converting whatever cryptocurrency you have into USDC on Polygon, for example. This makes it feasible for de-banked individuals to buy things the way most of the banked population does, without needing to get a bank account, which is no small feat.

It’s important to remember that payments you make using a Payy Card are associated with your legal identity. From that perspective, it’s not more private than a regular credit card. However, it is a lot more private than just using Bitcoin, Ethereum, or other transparent-ledger cryptocurrency systems directly, because your payments aren’t published publicly for the entire Internet to see.

Payy itself communicates what data is public and what data stays private when you sign up for a Payy Card.

I would not recommend using your Payy Card or the Payy network for any need you have that requires more privacy; do your best to stick with Zcash and Monero for that. However, if your friends are unwilling to adopt the stronger privacy protections offered by Zcash in Zodl, are scared of the volatility of actual privacy coins, or have otherwise succumbed to the propaganda that stablecoins are somehow superior (even though we know they’re not), Payy can be a convincing half-step to at least get them using cryptocurrency with you.

Your Payy Card can make you look more like a “normal” civilian in your personal life. And you can still keep your wealth private by having it in and moving it through the Zcash shielded pool (via Zodl) at every opportunity.

Opolis: a crypto-native independent employment platform

Opolis (referral link) is a novel digital employment cooperative you may be able to join (if you meet minimum income or eligibility requirements based on your needs, see below) that can offer a way to legitimize your income, including any earnings from cryptocurrency transactions. With Opolis, rather than work “under the table,” you set things up like a traditional business, funnel your earnings through that business, and then pay yourself back as a salaried employee.

In plain language, the whole setup works like this.

Register a legal business entity, such as an S-Corp that offers whatever services you provide.

You then hire yourself as an employee of that business, so you can pay yourself a salary out of the business’s future revenue.

Your business entity then partners (joins) with the Opolis business cooperative, which collectively negotiates employee benefits like health insurance plans.

Finally, your business in turn offers those employment benefits to you, the “human resource” (employee).

Yes, this tactic introduces complexity to your work. It means you have to go through the process of registering a business, like picking a name and choosing which State is best for you to register your business in. But the rubber meets the road when on-ramping the same as it did before, if not even better.

Getting paid directly in crypto is no different, just show a client your QR code from a cryptocurrency wallet.

You can use your registered business as a further shield to protect your individual privacy for accepting fiat payments like deposits when using your corporate bank account linked to fiat payment apps, notably Zelle. Just make sure you’ve registered your business in a privacy-friendly state like Delaware, Nevada, or Wyoming, and via a third-party registered agent so that you don’t have to list your legal identity as a publicly disclosed member of the corporation.

Now that you’re earning revenue on behalf of your business, you’ll need to record those funds in some accounting software. (I prefer to use GnuCash for this, but I’ve also heard good things about Rotki.) This way, you can treat it as your business’s taxable income for reporting when your business pays member dues in the cryptocurrencies Opolis supports.

A few other points to know about this off-ramp:

You don’t need to be earning all of your income from one aspect of your work to join. What matters is how much you’re making in total so that you (as a business) can afford to run payroll while covering operating expenses, employee compensation (salary and benefits), and paying taxes or other applicable fees.

Opolis can currently, subject to change, process payments in: DAI, ETH, BTC, USDC and USDT.

I’d love to hear about your experience if you try something like this so please don’t hesitate to reach out to me if you do!

Hopefully this guide gives you an idea of how you can use crypto to enhance your financial privacy. It may not be accepted natively everywhere yet, but that doesn’t mean that you can’t use it day-to-day anyway. In coming months we’ll talk about using wallets, and on-boarding into crypto as well.

Yours In Privacy,

Violet

Consider supporting our nonprofit so that we can fund more research into the surveillance baked into our everyday tech. We want to educate as many people as possible about what’s going on, and help write a better future. Visit LudlowInstitute.org/donate to set up a monthly, tax-deductible donation.

NBTV. Because Privacy Matters.